Data tokens on this page

Financial Solutions

Financial Solutions

Millennials and Money

A generation scared.

Jason P. Capone, CFP®

First Vice President

Wintrust Investments

Born between the early 1980s and mid-2000s, members of the Millennial generation have quickly become the largest, most diverse generation in the U.S., representing nearly one-third of the total population.1 On the heels of the Great Recession, many from this generation have spent their formative years in a period of unprecedented financial turmoil. For them, the financial crisis of 2008 and subsequent housing market collapse, and the two major stock market crashes of the past 15 years are the only impression they have of investing and home ownership. The resulting skepticism of the government and financial markets has adversely clouded Millennials’ financial judgment.

While studies show that Millennials are optimistic for the future—49% believe the country’s best years are ahead—their investing habits tell a different story.2 Despite the fact that younger investors have one of the cornerstones of successful equity investing on their side—time, and that historically, equities have rewarded investors handsomely over the long run, Millennials are forgoing market opportunity for perceived safety.

Last year, the average millennial investor held over half of their savings in cash (earning virtually nothing), and less than 30% owned stocks or stock funds. In 2013, Millennials in their twenties allocated only 41% of their defined contribution assets in equities, down from 62% in 2007.3 These data are also reflective of the investing habits of survivors of the Great Depression who tended to invest less and keep their savings in cash.

While keeping a majority of investable assets in cash may seem safe, there are significant opportunity costs. Despite the drastic market crash in 2009, an investment of $1,000 in the S&P 500 Index made in 2004 would have been worth $1,857 by the end of 2014. By comparison, a $1,000 investment in a cash equivalent such as 3-month Treasury bills over the same time period would have been worth only $1,165. Beyond avoiding equities, many Millennials are avoiding investing altogether. As of last year, only 73% of those in their twenties took advantage of their employers’ 401(k) programs, and nearly 40% of those failed to take full advantage of their employers’ company matching.4 This tendency to delay savings—as many Millennials have—is a costly mistake in the long-run.

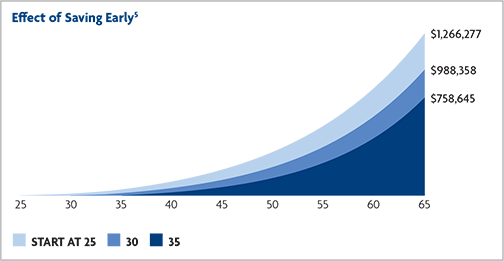

Consider, for example, a 25-year-old earning a $40,000 salary whose employer offers a 100% match on 401(k) contributions up to 5%. As the chart below illustrates, if the employee takes full advantage of the matching and contributes 5% beginning at age 25, he or she would have over $1.25 million in their retirement account by age 65.5 If the employee delays saving until age 30, they would have a quarter of a million dollars less in their account by age 65; and delaying until age 35 would leave them with little more than half of what they would have had if they had begun saving at age 25.

While Millennials’ apprehension towards investing and assuming market risk is completely understandable given their first impressions, the sooner they can over-come their misgivings, the sooner they can put compounding of interest and growing equity prices on their side. Millennials would be well served to embrace higher risk stocks as the driver of growth in their retirement portfolios. It may be a bumpy ride at times, but the long term reward will make the risk well worth taking.

One step towards that end is to talk to a Financial Advisor with Wintrust Wealth Management. They can help define financial goals, dispel investing myths and the unfounded fear that accompanies them, and implement an investment plan to help better ensure a sound financial future.

1. U.S. Census Bureau

2. Pew Research Study: www.pewsocialtrends.org/2014/03/07/millenials-in-adulthood/

3. UBS Investor Watch Survey, Q1 2014

4. Aon Hewitt

5. Assumes 7% annual return on the portfolio and 3% annual salary growth

Request an Appointment

Ready to start a conversation?

Call us at 630-655-8474 or:

Serving Clients At:

Jason P. Capone, CFP® also serves clients by appointment at the following locations: