Data tokens on this page

Financial Solutions

Financial Solutions

529 Education Savings Plans

A 529 Education Savings Plan can be an effective tool for investors seeking to save for education expenses.

Simply put, a 529 plan is a program that allows families to invest for education-related expenses on a federal income tax-free basis. They often also offer state benefits if you invest in a plan sponsored in by your state of residence. 529 plans are designed to pay for qualified expenses that include more than just tuition. Furthermore, anyone can open a 529 plan—parents, grandparents, family, friends. 529 plans were established in 1997 when Congress passed legislation that created qualified state tuition programs under Section 529 of the Internal Revenue Code. The intention was to provide tax incentives to families trying to meet the high cost of a college or post-graduate education. Qualified expenses also include up to $10,000 per year per beneficiary for tuition at an elementary or secondary public, private, or religious school.

Overview

What Are the Main Benefits?

Contributions in most 529 plans grow entirely tax free, meaning no capital gains taxes are paid. About half of states offer tax deductions on contributions in their 529 plans.

Who can contribute?

Anyone, regardless of income, can contribute, whether the 529 plan is for their child or that of friend or family member.

How are prepaid plans and savings plans different?

529 prepaid plans are contracts that you purchase to lock in today’s tuition rate at public and some private colleges in a particular state. Restrictions apply when using funds in 529 prepaid plans for out-of-state colleges and the impact on financial aid is more severe than if you invest in 529 savings plans.

529 savings plans are made up of mutual funds that grow tax-free and can be used for any qualified higher education costs, such as tuition, room and board, and other college expenses.

What is the minimum and maximum investment?

Minimum investment amounts vary from state to state, but you can invest as little as $25 to open a 529 plan and make subsequent contributions as little as $10. Maximum asset limits for 529 plans also vary by state, ranging from $235,000 to $550,000, and represent what the state believes to be the full cost of attending an expensive school and graduate school, including textbooks and room and board. While the IRS does not specify annual contribution limits to 529 plans, some consideration should be given to gift and estate tax laws.

What options do I have?

There are now over 700 different investment options, with many well-known fund managers such as Fidelity, AllianceBernstein, American Funds, Vanguard, and Merrill Lynch. Plus, there are more than 75 different 529 plans from which you can choose.

What costs are associated with investing?

529 plan costs range from 0%–2.5% of your assets per year, plus some front- and/or back-end sales fees. For example, if you have $100,000 invested and the expense ratio is 1.5%, you pay $1,500 that year. This is a standard practice in the mutual fund industry. The states that govern the plans and the fund managers are compensated for administering the plan and managing your money. Selecting plans with lower expense ratios is generally a smart strategy, although how a plan performs also affects the returns on your investments.

In-State and Out-of-State Plans

Each state sponsors its own plan, and some states have multiple plans. One of the most important things to consider is the firm providing the investment management services and the performance, fees, and asset allocation options they offer. You may also enjoy reduced fee levels if you already invest in funds from the manager.

In Illinois, there are two plans—Bright Start and Bright Directions. There are also two plans in Wisconsin—EdVest and Tomorrow’s Scholar1. Remember though, that using a specific state’s 529 plan does not mean the funds have to be used for education expenses in that state, rather they can be used to pay for qualified education expenses in any state.

529 Plan Advantages

Earnings grow federal income tax free

529 plans allow the assets in your account to grow free of federal income tax. This is not an option with other types of minor accounts, such as Uniform Gifts to Minors Accounts (UGMA) and Uniform Transfers to Minors Accounts (UTMA). In these account structures, earnings are taxed at the parent’s or minor’s rate.

Qualified withdrawals are free from federal income tax

Withdrawals from a 529 plan, when used for qualified expenses, are also free from federal and state income tax. Qualified expenses typically include tuition, books and fees, as well as room and board when attending at least half time. Keep in mind that the definition of qualified expenses may vary from state to state and is also subject to change.

Contributions receive favorable gifting and estate tax treatment2

Contributions to a 529 plan can help you avoid gift and estate taxes under certain circumstances. You can contribute up to $80,000 per beneficiary in a single year, or $160,000 for married couples, without federal gift tax consequences, provided that no additional taxable gifts are made to the beneficiary over a five-year period. Additionally, contributions made to a 529 plan are excluded from your taxable estate for federal estate tax purposes. It is important to note that this exclusion is subject to an add-back rule in the event of death within five years. Furthermore, while rules vary from state to state and even though your contributions are not deductible on your federal tax return, some states offer an income tax deduction if you invest in that particular state’s sponsored plan. In Illinois, you can deduct contributions on your state tax return up to $10,000 for single filers or $20,000 for those filing jointly. In Wisconsin, you can deduct contributions on your state tax return up to $3,380 per beneficiary per year. Contributions in excess of $3,380 may be carried-forward to be applied in subsequent tax years.

No age or income restrictions

You can establish a plan regardless of how much you earn for a beneficiary of any age.

Control over assets

One of the greatest advantages of a 529 plan is that when you open an account, you have control of the money. The beneficiary never has access to the funds and they are intended solely for qualified, higher education expenses.

Wide range of colleges and technical programs

Freedom of choice means you can choose from a wide selection of colleges. The student can attend any university or college within the United States or abroad that the U.S. Department of Education has defined as an Eligible Educational Institution. Furthermore, the assets in the 529 plan can be used to fund post-graduate degrees as well.

Professional investment management

The assets in the plan are managed by an independent, professional money manager selected by the state that sponsors the plan.

Low contribution requirements and high contribution limits

With a 529 plan, you can vary your contribution amount based on your situation. Plans often have a low initial contribution requirement. Total plan contribution limits vary by state: currently $500,000 in Illinois and $527,000 in Wisconsin for example, for any one beneficiary over the life of the plan. This could be an effective means for you to accumulate assets quickly to fund college and possibly transfer part of your personal estate in a tax-advantaged way. Also anyone can contribute—parents, grandparents, or friends of the family.

Ability to change beneficiaries

If the designated beneficiary chooses not to attend college, the 529 plan owner can designate another member of the beneficiary’s family as the beneficiary. Furthermore, the definition of family member can extend to first cousins and step-children.

Choosing an Investment Approach3

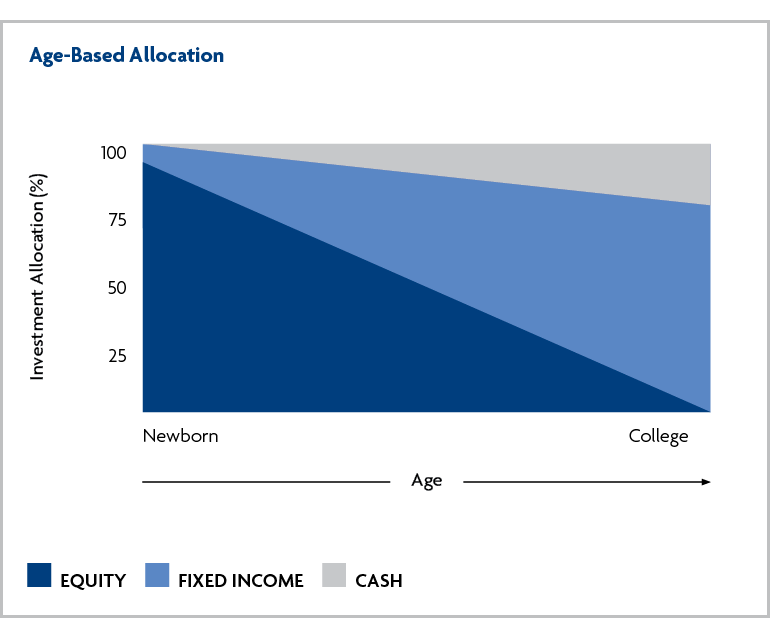

Age-based asset allocations

Many 529 Plan providers offer Age-Based Asset Allocations which enable you to select an asset allocation track suitable for your needs. Investments will be placed in a portfolio within the asset allocation track chosen based on the beneficiary’s age. As your beneficiary ages, the age-based allocations are designed to reallocate a percentage of the assets out of equity-based funds (primarily stocks) into more conservative, income-seeking funds (such as bond and money market funds). By the time college is around the corner, a greater proportion of your assets will be in more conservative, lower-risk investments.

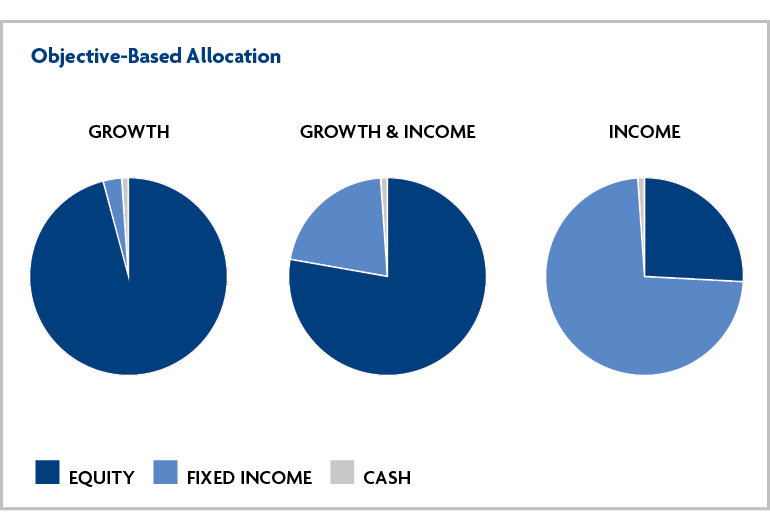

Objective-based allocations

Objective-Based Asset Allocations allow you to invest your assets according to the amount of risk with which you are comfortable taking and the potential return characteristics you prefer. The number of objectives offered varies from plan to plan as do the portfolio names, but typically will range from aggressive to moderate to conservative:

- “Growth” is often used to describe an allocation designed for investors with a longer investment time horizon and a higher tolerance for risk.

- “Growth & Income” is a common name for a moderate allocation designed for investors who have a longer to medium time horizon and can tolerate a moderate amount of risk.

- “Income” is a typical label for a more conservative allocation designed for investors with a shorter to medium time horizon and are comfortable with a lower amount of risk.

Unlike age-based allocations, these do not change over time automatically, but maintain a relatively constant investment mix designed to meet the risk-return needs of the investor. As the need to make withdrawals draws nearer, you may consider changing your investment objective to more conservative allocations.

Individual investment allocations

Some 529 plans allow you to choose individual investment options and allocations as you see fit. Many plans have included multiple managers, giving the investor the option to choose from ‘best of breed’ investment managers including firms such as PIMCO, Vanguard, Fidelity, American Funds, and Franklin Templeton.

Getting Stated With a 529 Savings Plan

It is important to realize there are a variety of education savings plans available to investors. To determine if a 529 plan is right for you and to start saving today, contact a Financial Advisor with Wintrust Wealth Management.

1. Bright Start and EdVest are available as client/self-directed programs.

2. Tax benefits are conditioned on meeting certain requirements. Federal income tax, a 10% federal tax penalty, and state income tax and penalties may apply to non-qualified withdrawals of earnings. Generation-skipping tax may apply to substantial transfers to a beneficiary at least two generations below the contributor. Gift examples are general; individual financial circumstances and state laws vary—consult a tax advisor before investing. If the contributor dies within the five-year period, a prorated portion of contributions may be included in their taxable estate. See a 529 disclosure document for more complete information.

3. An investment in a 529 Education Savings Plan is an investment in a municipal security that may invest in one or more underlying mutual funds. It is not an investment in shares of the underlying mutual fund(s). Asset allocation, diversification and rebalancing do not guarantee a profit or protect against loss.

Start the Conversation

Where will your financial journey take you? A Financial Advisor helps you navigate the terrain, avoid pitfalls, and keep you on track to achieve your financial goals.